Page 13 - NBIZ Magazine April 2022

P. 13

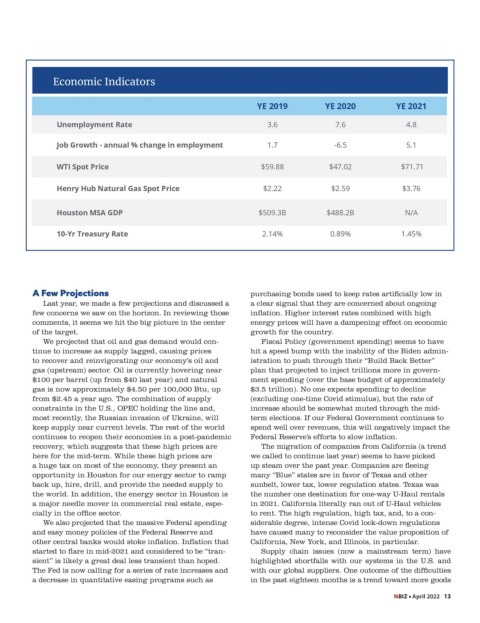

Economic Indicators

YE 2019 YE 2020 YE 2021

Unemployment Rate 3.6 7.6 4.8

Job Growth - annual % change in employment 1.7 -6.5 5.1

WTI Spot Price $59.88 $47.02 $71.71

Henry Hub Natural Gas Spot Price $2.22 $2.59 $3.76

Houston MSA GDP $509.3B $488.2B N/A

10-Yr Treasury Rate 2.14% 0.89% 1.45%

Population

A Few Projections purchasing bonds used to keep rates artificially low in

Last year, we made a few projections and discussed a a clear signal that they are concerned about ongoing

few concerns we saw on the horizon. In reviewing those inflation. Higher interest rates combined with high

8.5

comments, it seems we hit the big picture in the center energy prices will have a dampening effect on economic

Millions

of the target. growth for the country.

8.0

Fiscal Policy (government spending) seems to have

We projected that oil and gas demand would con-

7.5

tinue to increase as supply lagged, causing prices hit a speed bump with the inability of the Biden admin-

to recover and reinvigorating our economy’s oil and istration to push through their “Build Back Better”

7.0

gas (upstream) sector. Oil is currently hovering near plan that projected to inject trillions more in govern-

$100 per barrel (up from $40 last year) and natural ment spending (over the base budget of approximately

6.5

gas is now approximately $4.50 per 100,000 Btu, up $3.5 trillion). No one expects spending to decline

from $2.45 a year ago. The combination of supply (excluding one-time Covid stimulus), but the rate of

6.0

constraints in the U.S., OPEC holding the line and, increase should be somewhat muted through the mid-

most recently, the Russian invasion of Ukraine, will term elections. If our Federal Government continues to

5.5

keep supply near current levels. The rest of the world spend well over revenues, this will negatively impact the

5.0

continues to reopen their economies in a post-pandemic Federal Reserve’s efforts to slow inflation.

recovery, which suggests that these high prices are The migration of companies from California (a trend

2008 2010 2012 2014 2016 2018 2020 2022 2024 2026

here for the mid-term. While these high prices are we called to continue last year) seems to have picked

a huge tax on most of the economy, they present an up steam over the past year. Companies are fleeing

opportunity in Houston for our energy sector to ramp many “Blue” states are in favor of Texas and other

back up, hire, drill, and provide the needed supply to sunbelt, lower tax, lower regulation states. Texas was

Jobs

the world. In addition, the energy sector in Houston is the number one destination for one-way U-Haul rentals

a major needle mover in commercial real estate, espe- in 2021. California literally ran out of U-Haul vehicles

cially in the office sector. to rent. The high regulation, high tax, and, to a con-

We also projected that the massive Federal spending siderable degree, intense Covid lock-down regulations

Jobs Gained Jobs Lost

Forecast

and easy money policies of the Federal Reserve and have caused many to reconsider the value proposition of

other central banks would stoke inflation. Inflation that California, New York, and Illinois, in particular.

200,000

COVID-19 Recovery

started to flare in mid-2021 and considered to be “tran- Supply chain issues (now a mainstream term) have

Shale Gas & Oil Boom

150,000

highlighted shortfalls with our systems in the U.S. and

sient” is likely a great deal less transient than hoped. 116,700 151,800

117,500

106,900

The Fed is now calling for a series of rate increases and with our global suppliers. One outcome of the difficulties

82,700

100,000

82,900

91,000

62,200

a decrease in quantitative easing programs such as in the past eighteen months is a trend toward more goods

75,500

54,200

50,000 50,500 90,000

21,500 -2,500 -2,400 NBIZ ■ April 2022 13

0

-50,000

Energy Downturn

-100,000 -110,500

-150,000 The Great Recession

-200,000

COVID-19 Pandemic -206,600

-250,000